I’m the owner of a small Internet company that’s qualified for the maximum $100,000 Kabbage loan. Before applying for Kabbage I was searching for a genuine Kabbage loan review but couldn’t find one. I was starting to look into Kabbage because I’d recently been fueling our growth with business loans rather than going back to the venture capital world where we previously raised $550,000. Even with high interest rates, these loans are cheap when compared to selling equity in the company.

Why does any of that matter?

I want you to know this isn’t a handpicked testimonial or a case study from Kabbage’s website. Those are great, but they always leave you wondering if they’re legit or not. What follows is an unbiased, comprehensive Kabbage review from a business owner. It’s not some quick pros and cons list, but rather a deep-dive into the product and my entire experience qualifying for the maximum $100,000 line of credit.

But before I dive into all that let’s talk about how I decided to even start considering Kabbage at all.

Why I began evaluating Kabbage

Over the last couple years I’ve taken two PayPal loans via their Working Capital program. In my comprehensive PayPal loan review, the program scored an impressive 26.5/30.0, or 88%. Clearly, I’ve been quite happy with the program. So why even consider shopping around?

For starters, you should always evaluate your options from time to time. As a smart business owner you no doubt know that already. But beyond that, there are elements of PayPal’s working capital program that need improvement. Furthermore, my ten-year-old bankruptcy had finally fallen off my credit report and I was now boasting a near 800 credit score. So I was feeling pretty confident that if I applied for a loan, I’d get a pretty decent rate.

Kabbage loan review criteria

If you aren’t familiar with Kabbage yet, I’m going to start with a brief overview of their offering and what it takes to qualify. Then I’ll review the program on six criteria, ranking them on a scale of 1-5: ease of application, fees & rates, structure & repayment, sales pressure, speed of funding, and loan amount.

This is the type of Kabbage review I wish I could have read before applying. My hope is that it’s comprehensive, but if you feel like I’ve missed something, please give me a shout in the comments so I can add it. Let’s get started.

Kabbage loans: What it is and how to qualify

Kabbage offers a business line of credit. This is different than a loan, so it’s important to make that distinction. I’ll get more into how the line of credit works later in the review and why it’s more flexible. Like most small business loan providers, the line of credit is meant to be used for working capital. This can be anything from purchasing inventory to ramping up your labor force.

Whatever you draw from the line of credit is paid back as a loan on a monthly basis either over a six-month or twelve-month timeframe. Payments are fixed, so you always know what you owe each month.

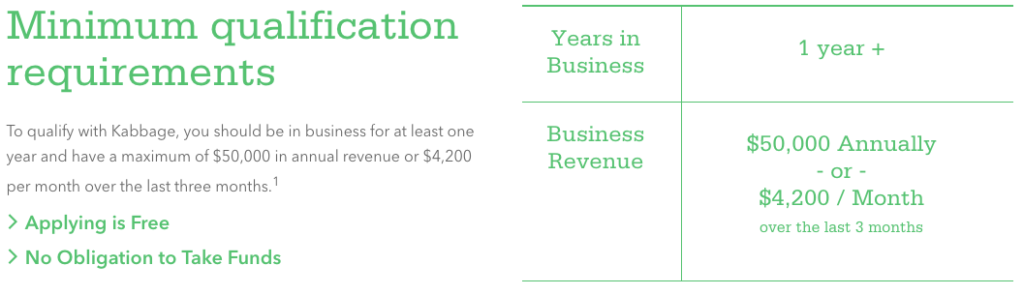

Like most business loan lenders, Kabbage has some upfront qualifications: you have to have been in business for at least a year and you must have $50,000 in revenue annually or $4,200 per month for the last three months.

Kabbage loan review: Ease of application

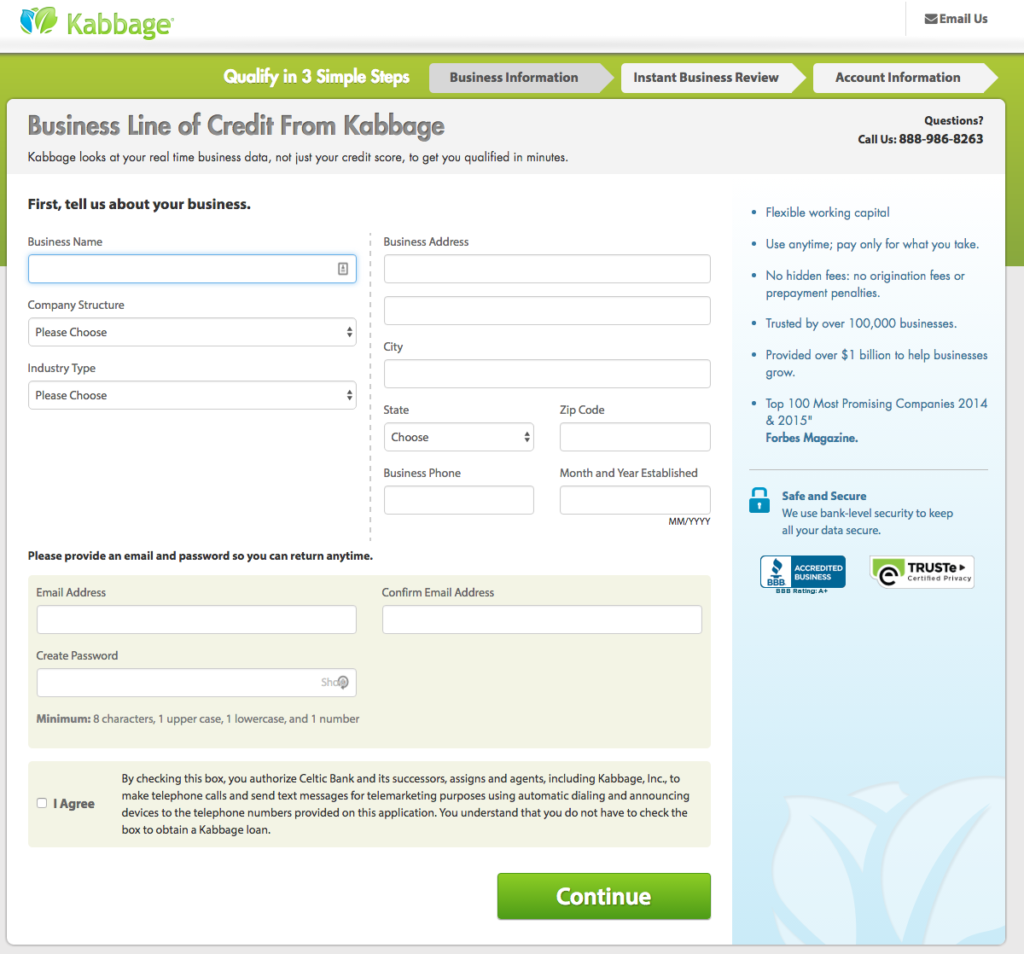

Kabbage loans are incredibly easy to apply for. To start, you fill out some general information about your business:

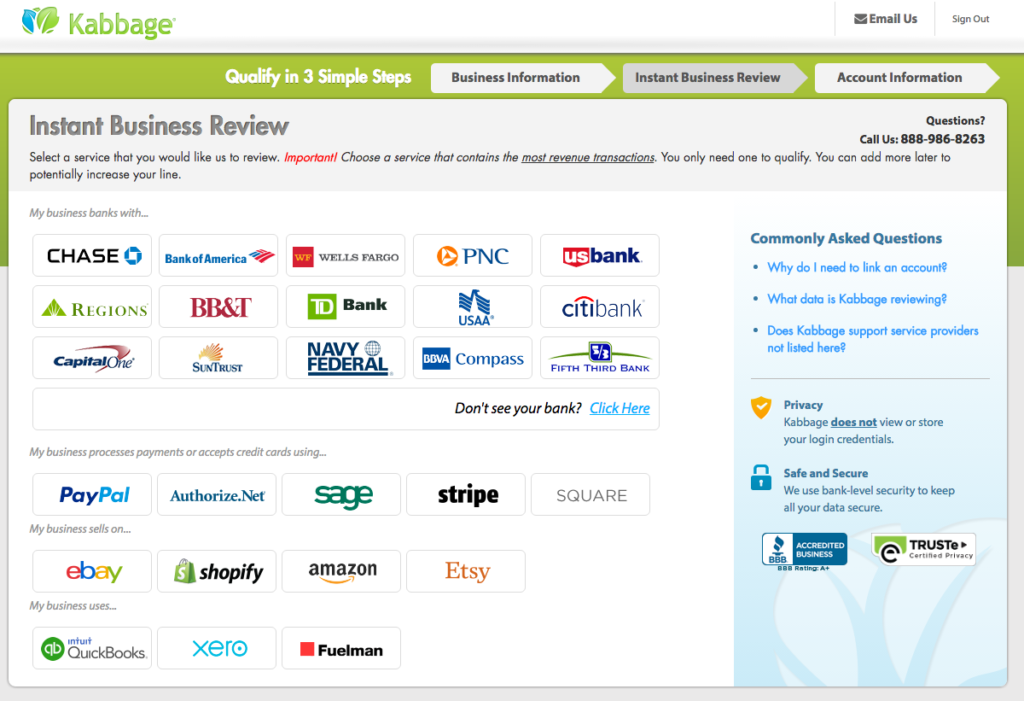

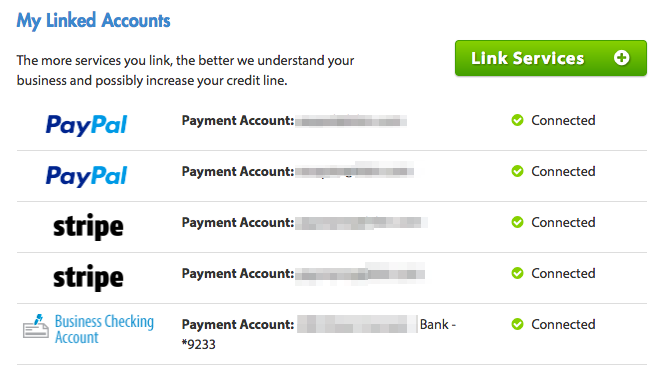

Once you fill in the information and click ‘continue’, you’ll be asked to connect your business accounts. Kabbage encourages you to connect accounts with the most transaction volume, and this makes sense. The line of credit you’re approved for is largely dependent on how much revenue you generate. So take some time and connect as many accounts as possible.

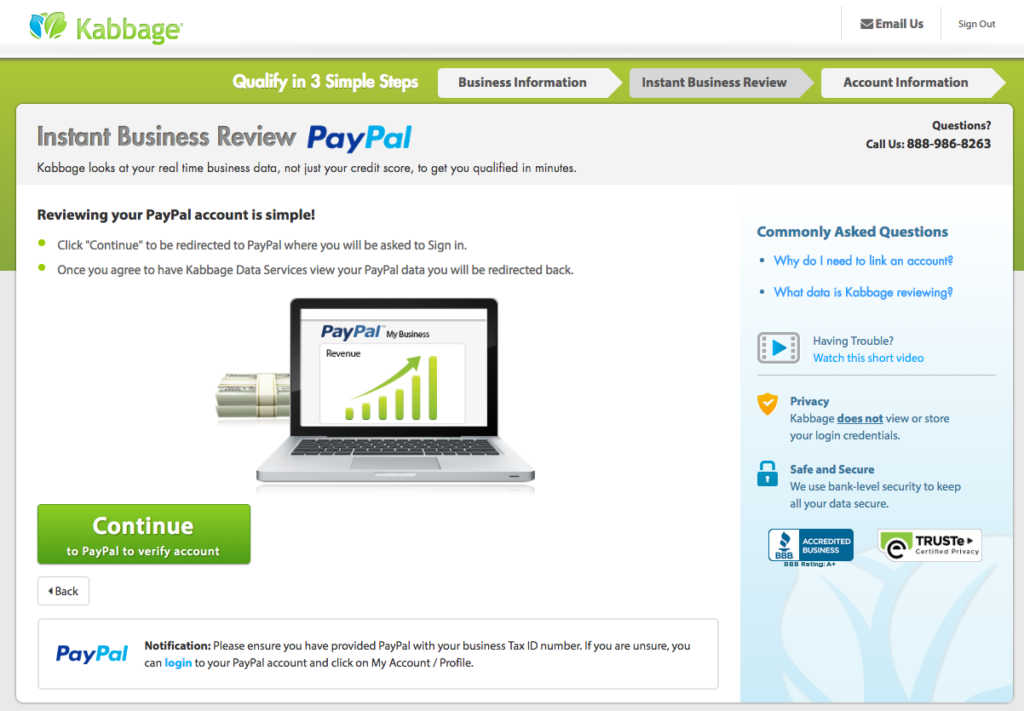

Example of connecting a PayPal account

My business processes a lot of transactions via PayPal, so we’d obviously want to connect that account. After clicking on the PayPal icon you’re directed to a new page:

Once you click the ‘continue’ button you’re immediately redirected to PayPal where it will ask you to login to your account. Upon logging in you’ll see a request for access to your PayPal history. It will look like this:

Once you grant permission you’ll be redirected back to your Kabbage dashboard. You’ll want to add as many accounts as you can. The better profile you give Kabbage about your business and the revenue you generate, the more they’ll likely be able to qualify you for.

My company has several PayPal accounts and we also process transactions via Stripe. And of course, we added our bank account too:

Once you’ve connected all your accounts Kabbage will be able to tell you how much of a loan you’ve qualified for and at what rates. Overall, the application process is quite easy. It takes some time connecting your accounts, but Kabbage never asks for documentation, or makes you jump through hoops. In terms of ease of application, I give it a perfect score.

score: 5/5

Kabbage loan review: Fees & rates

You don’t need to apply for a Kabbage loan by signing up and connecting your accounts to start understanding how Kabbage charges fees & rates on their lines of credit. That’s something I really appreciated when digging into their website. To get an idea of what Kabbage loans cost they’ve created a page to help simulate different loan amounts with the payback options.

For example, they show a $100,000 loan on a 12-month payback period would cost a total of $24,000 in fees. That’s a bit expensive, but given the ease of application and the ability to potentially get a business loan fast, it’s reasonable.

I can also tell you from experience that a 24% APR is relatively competitive. I’ve taken PayPal Working Capital loans and their APR generally falls around 21%. You can see my deep-dive PayPal loan review here. I’ve also applied for an OnDeck loan, and their APR came in at a whopping 29% (review coming). So 24% is reasonable when comparing against competitors. And that in itself was enough to get me interested in seeing what we might qualify for.

But then I saw this:

The important part is:

“Fee Rates range from 1.5% to 10% based on a number of business performance factors. Apply to find out what your Fee Rate could be. “

Kabbage fees were a pleasant surprise

This wasn’t insanely clear, but it seemed like you could potentially qualify for a loan with an even lower APR than the quote in the slider. And once I linked all of our accounts, that’s exactly what I found:

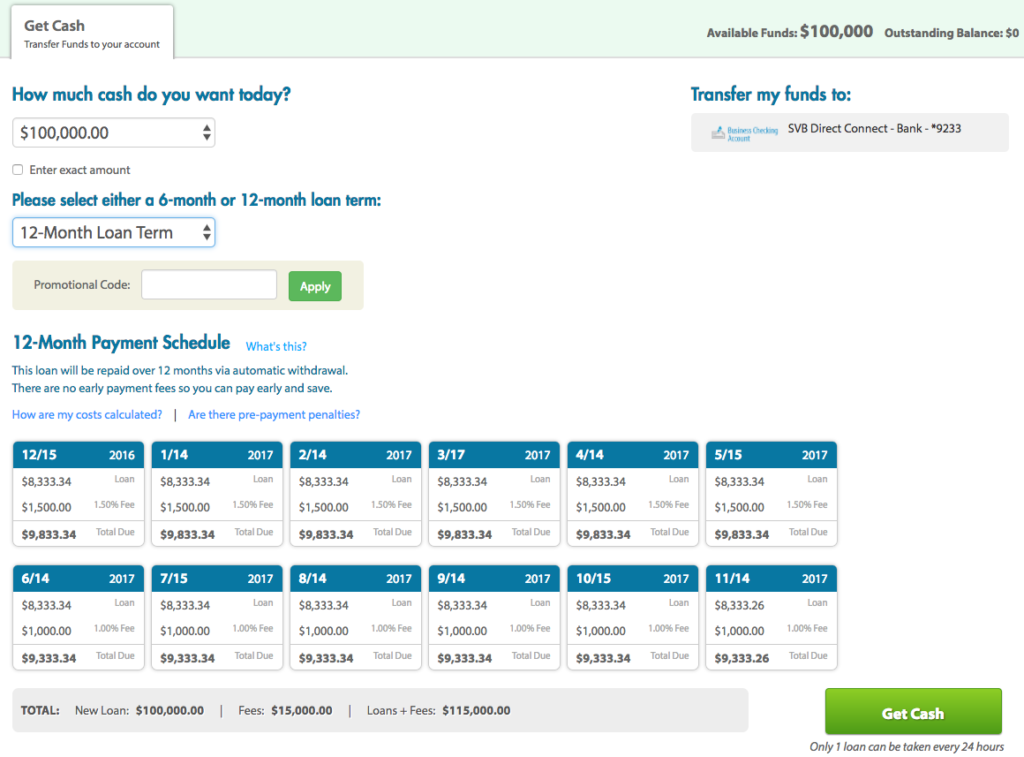

As you can see, we qualified for a $100,000 Kabbage line of credit with the lowest fees possible. If we took the full $100,000 and paid it back over 12-months we’d pay $15,000 in fees, or 15% APR. Paid back over 6-months and it’d be $7,000 in fees, or 14% APR. Remember, the slider tool on Kabbage’s website was showing us $24,000 for 12-months and $10,000 for 6-months on a $100,000 loan.

It’s rare that you are positively surprised by a business loan provider. Often they’ll tout their lowest rates and fees to get you in the door and then qualify you for something wildly different. I’m not saying everyone’s experience will be like mine (my business generates a fair amount of revenue and I have very strong credit now), but the pleasantness of this experience should not go unmentioned.

While a 14% or 15% APR may not be attractive when compared to something like a mortgage or traditional loan from a bank, it’s quite attractive in the working capital loan space. Remember, this is an unsecured loan and they don’t require any paperwork or drawn out processes to get the cash you need. When it comes to fees and rates, Kabbage has been by far the most attractive option I’ve seen. How can I give it anything but a perfect score?

score: 5/5

Kabbage loan review: structure & repayment

Our third criteria for evaluating business loan lenders, in this case the Kabbage loan, is the loan structure. Specifically, we want to look at what the payback terms are. Some lenders waive your fees if you repay the loan early while some lenders don’t. You also want to make sure that you aren’t agreeing to a repayment schedule that’s not feasible for your business.

How Kabbage loans are structured

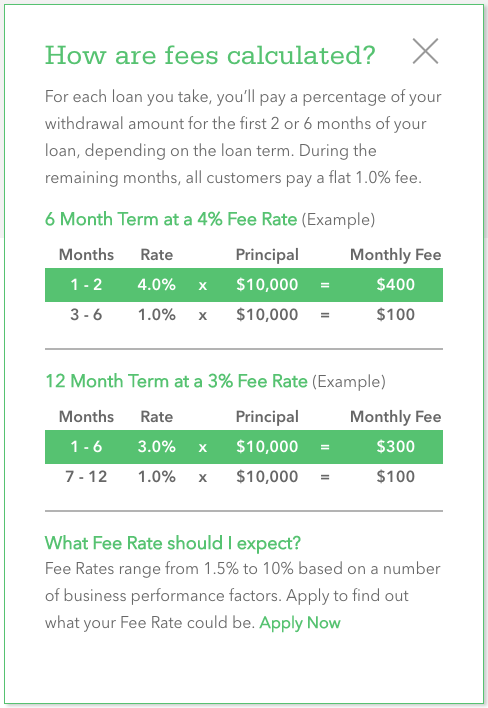

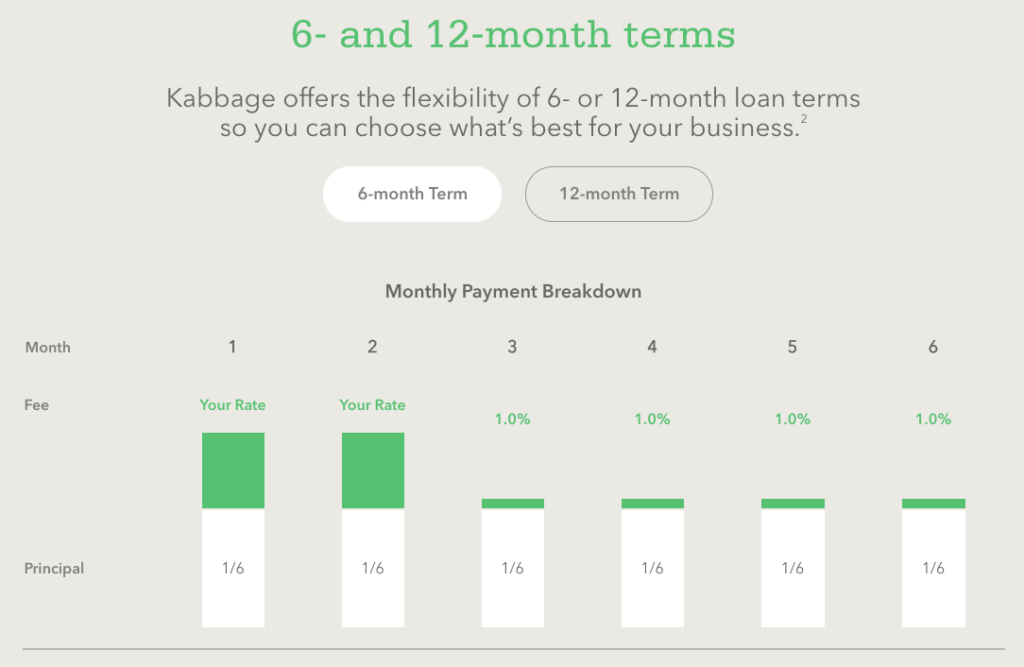

We already know that the Kabbage loans are structured with a set fee. The fee is determined algorithmically based on your transaction volume, your bank account balance, and your credit score. All this is obtained by linking your accounts during the application process.

But the fee you pay is actually a monthly fee as a percentage of how much you choose to borrow. This fee is higher in the first two to six payments you make than it is the last four to six payments. Essentially, you pay a fee each month to borrow money from Kabbage. Kabbage recently redid their site to better depict the fees. Here’s a great graphic:

That’s still a bit confusing, I know. Let’s look at an example in the next section.

How Kabbage loans are repaid

When you draw from your Kabbage line of credit, you’re essentially paying a monthly fee to hold that money. Think of it like a rental fee. You’re paying to rent the use of capital. And each month that capital is partly paid back along with the respective rental fee.

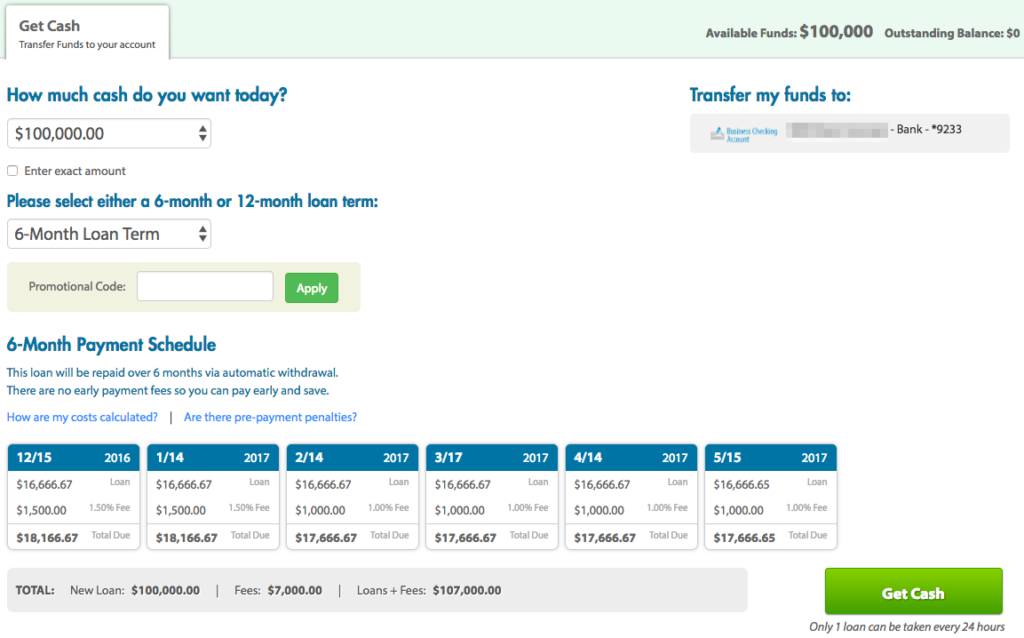

Kabbage gives you two loan term options: a 6-month payback period and a 12-month period. If you opt for the 6-month structure, you’ll pay a higher fee for the first two months and then a lower fee for the last four months. Here’s a screenshot of a $100,000 loan that my business qualified for:

The fee we’d pay in month’s one and two is 1.5%. After that it drops to a flat 1.0%. The 12-month loan has the same structure except the 1.5% fee spans the first 6-months before the fee drops to 1.0%. Notice the fee is always presented as a percentage of the original loan amount.

But you don’t necessarily have to end up paying the entire fee shown for your loan.

Early repayment

If, for whatever reason, you decide or are able to repay your Kabbage loan early, you don’t pay fees on the remaining duration of the loan. Remember our liking it to renting capital. If you return the capital early, you’re no longer paying a rental fee.

So, for example, if I paid the above 12-month, $100,000 loan off in 6-months instead of the full 12, I’d save the last $6,000 in fees. That means I only end up paying $9,000 instead of the original $15,000 fee.

Why does Kabbage do this?

Not all business loan lenders allow you save on fees when you repay loans early. For instance, PayPal Working Capital doesn’t. But notice what Kabbage has done here. By front loading higher fees in the beginning of your repayment schedule, Kabbage is guaranteeing themselves a higher effective APR.

Paying $9,000 in fees in 6-months to borrow $100,000 is an effective APR of 18%. If you’d waited the full 12-months to repay the loan, the effective APR is just 15%.

In fact, if you repay your loan early at all, Kabbage earns a higher APR than what they would if you paid the loan back over the full duration of the loan.

Does this mean it’s a bad idea to repay your loan early?

Absolutely not.

While I think it’s important to understand the true cost of the money you’re borrowing (and calculating the APR is the only way to do that), Kabbage has essentially set up a win-win.

After all, you’re paying less in fees. Are you really going to not repay your loan early (assuming you were in the position to), and pay more in fees, just so you can say you paid a lower APR?

I sure hope not!

Makes sense, but what’s in it for Kabbage?

Simply put, if you repay your loan early, Kabbage can loan that money out again to someone else right away. Had you waited to pay it back over the full duration of your loan, well, then Kabbage has to wait to loan it out.

Everyone’s happy!

Structure & repayment conclusion

Overall, I really like what Kabbage is doing. They keep things simple, offering two loan structures: six or twelve months. They make it insanely easy to see exactly what you’ll be repaying and when. Furthermore, they’re very transparent about their fees.

There’s really nothing to dislike here, and it’s why, once again, Kabbage scores perfect in this category.

score: 5/5

Kabbage loan review: Sales pressure

There are few things I hate more in life than having my phone light up with a bunch of cold calls.

Ugh.

So I thought it appropriate to include this as a criteria. I don’t know anyone that enjoys pushy sales people. Heck, that’s why I tend to do a ton of research on the Internet before making large purchase decisions, so I don’t have to talk to someone!

When I applied for a loan through Kabbage I was immediately sent an email from a gentleman that was my “new account manager”. It’s nice to have a point person that can answer questions or help resolve issues quickly, so I appreciated that. But how was interacting with my account manager in general?

Account manager interaction

My account manager, let’s call him Dave (not his real name), was friendly and eager to get us started with our loan. He was quite excited because we’d been approved for the largest Kabbage loan possible ($100,000) and the minimum fees. Once all my questions had been answered and the account to have funds sent to was changed to our bank account rather than a PayPal account, he got right down to business. He said,

“When do you think you’ll be drawing on your line of credit?”

I explained to Dave that I wasn’t quite sure, but it would be relatively soon, likely within the week. And at the time, that was the truth. I wanted to run some numbers in our financial projections and see what impact having an extra $100,000 on hand could have. I planned to do that over the weekend and told Dave I’d likely know Monday or Tuesday.

Dave gets more aggressive

I didn’t expect to hear from Dave until at least Monday afternoon (if at all), but before I left for the office on Monday morning I already had an email and a missed call from him. It wasn’t even 8:00am my time yet!

I emailed Dave back, explaining that I wasn’t sure yet when we’d draw on the Kabbage line of credit. He replied saying he had a promotion code, but he couldn’t send it to me via email… it had to be over the phone. I ignored it.

The rest of the week I received both phone calls and emails from Dave. I talked to him once or twice, again explaining we weren’t quite ready to draw on the line of credit. And he provided me the promotion code, a $250 gift card if we took a loan for the full $100,000.

Side note… A $250 gift card isn’t going to have any impact on my decision. Especially considering we’d be paying thousands of dollars in fees on the Kabbage loan itself.

In the end, I ducked most of Dave’s calls and ignored his emails until I finally got fed up and specifically asked him not to contact me any longer. I told him I’d contact him when we were ready to proceed and thanked him for his time.

Sales pressure conclusion

It’s clear that Kabbage account managers are at least partly compensated on how much their customers draw on their lines of credit. Dave was pretty aggressive and relentless, something I didn’t appreciate. That said, he did back off when I specifically told him to. I have a hard time saying no and disappointing people. I could have probably told him to back off much sooner than I did.

Overall though, I really dislike sales pressure. Until this point, Kabbage had a perfect score. But I have to knock a point off for this category.

score: 4/5

Kabbage loan review: Speed of funding

Getting quick access to your loan is an important factor, and it’s something that’s not difficult to solve. Having funds in your bank account in one business day isn’t too much to ask. And anything longer than 2-3 business days just shouldn’t happen.

Kabbage does a fine job of getting cash to your designated account. We had our bank account hooked up to be the account for line of credit draws to be sent to, and funds were received in the 2-3 day window they promised.

Our account manager, Dave, was also good about letting us know to be sure to request draws a few days before you need them. There was nothing surprising here, and delivery of funds falls within my expected timeframe. Easy enough!

score: 5/5

Kabbage loan review: loan amount

When shopping different business loan providers, one things I discovered was that the amount of funding you qualify for can vary wildly. I applied with PayPal Working Capital, Kabbage, and OnDeck all in the same day. If you read my PayPal loan review you know that we qualified for $36,000.

That’s just over a third of what we qualified for with the Kabbage loan… $100,000! Crazy, right?

Kabbage’s maximum loan offering

The maximum Kabbage will ever loan a company is $100,000 which is $15,000 higher than the most PayPal will loan your business. The slightly larger loan potential was one of the reasons I decided to apply with Kabbage. And I’m glad we did. We qualified for the full $100,000!

One thing I would love to see is Kabbage offer even larger loan amounts. The good news? That’s apparently (according to our account manager, Dave) already in the works. Dave told me that Kabbage is starting to work with a small group of businesses to offer up to $200,000 and if we took the full $100,000 line of credit it’d be a “great signal” to Kabbage that we’re a business that could benefit from more capital.

This could have just been a sales pitch (and likely partly was), but I hope there’s some truth to it. If you’re a responsible, well run business, the more access to capital you have the better! Overall I was exuberant when we qualified for the full $100,000 line of credit after we didn’t come close to that with PayPal loans. So for now I’m still extremely happy with the Kabbage loan amount.

score: 5/5

Kabbage loan review conclusion

Overall, the Kabbage loan program is extremely strong with an overall score of 29.0 out of a possible 30.0; that’s a (rounded) 97%, or strong A grade. The only spot they lost a point was in the “Sales Pressure” category. So if you don’t mind aggressive sales people, or have no problem telling them off quickly, you may not care.

Kabbage loans are quick and easy to qualify for, and I was surprised with how much we did qualify for compared to other business loan lenders. Funds arrive in your account of choice quickly, and the repayment is as clear as day. They do a great job of showing you exactly what you’ll have to repay and on what kind of schedule.

APR is still a bit high, but again… that’s expected with these types of loans. That said, Kabbage loans have offered the most competitive APR of any business loan provider I’ve applied with so far. I’d like to see Kabbage up their potential loan amount even more, but that’s hardly something to complain about. And again, this is something they are supposedly experimenting with already.

I have almost no complaints with Kabbage and their loan offering. I highly recommend them to any business that’s in need of working capital. If you’re ready to get started with Kabbage, click here!

Super complete article. Love all the screenshots that walk me through the process of applying for a Kabbage loan. Our small business has need of a line of credit for working capital and I am applying today to Kabbage. After reading your post it all makes sense. I was confused about how they evaluated my credit but now I see they review my online accounts and my actual revenue and transactions. Thank You

Marsha, glad you found the article so useful. I’m biased, but I believe it to be the best and most comprehensive Kabbage review available. That said, if there’s something you think I missed or you have further questions, I’m happy to help! Just let me know.