Ten years is a long time to wait for something to happen. When that something is a bankruptcy falling off your credit report it can feel like eternity. I filed for bankruptcy in 2006, and as my ten year anniversary approached, all I wanted to know was what kind of credit score change I would see once my bankruptcy was removed.

Related: How long does a bankruptcy stay on your credit report.

I can remember as far as six months before the expected bankruptcy removal, Googling to find first hand accounts of people’s scores skyrocketing after their bankruptcy was removed.

Credit score change horror stories

But that’s not what I found. Instead, I was horrified. Rather than reading celebratory stories of massively positive credit score changes, it was just the opposite. I found this thread on CreditKarma that detailed dozens of stories of people that experienced a negative credit score change after their bankruptcy was removed. Here’s one of the posts from the forum thread:

“I just had my approximately 10 year old bankruptcy drop off my Experian report (it is still on my TransUnion and Equifax). My Experian score went from 721 to 680 overnight (down 41 points), while the other two scores remained relatively the same. I can’t wait to see how my bankruptcy DROPPING OFF will effect my other two scores, jeeze!”

And another poster:

“My score dropped 38 points after the bankruptcy came off. Credit scoring is a joke.”

What the heck… how can this be?!?!

One poster seems to have the answer, and I’ll admit… he had me pretty convinced:

“It doesn’t increase. After your BK is removed you are grouped with others who haven’t filed BK, so your FICO will go down. The sooner you started rebuilding credit after your discharge, the softer the blow.

So for people who are in BK your score is based on other people who are in BK. Once your BK is removed your score is based on other people who have no BK on their record. That’s why your score decreases, it makes sense since people in BK on average have lower scores than people who don’t have BK.

Hope that helps!”

Surely, this can’t be right… can it?! More searching led to yet another bankruptcy removal discussion thread. The general consensus was the same: Expect your credit score to drop after your bankruptcy is removed.

Yikes!

Waiting for my credit score change

I had visions of a huge jump in my credit score come October 2016, but that dream was now unraveling as I read these anecdotes. Sure, there were a few people chiming in that their scores went up. But they seemed to be the exception, not the rule. Suddenly I was left wondering how bad my credit score would be impacted once I was now being compared to this new “bucket” of individuals.

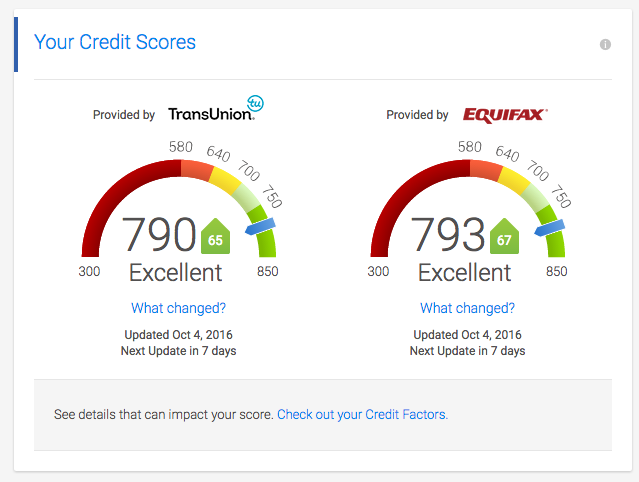

So I anxiously awaited the day my bankruptcy would fall off my credit report. And when that day came, here’s what I was greeted with in my CreditKarma dashboard:

I can’t even begin to describe the relief I felt at this moment. So what’s the deal, why are so many people on credit forums reporting a negative credit score change?

There are no mythical “buckets”

First, be careful about taking anonymous forum posts as voices of authority. The guy that was claiming he had the answers for why people were seeing lower scores after their bankruptcy fell off clearly has no idea what he’s talking about. I’ll admit, it got me thinking, but in the end I was skeptical this was in fact true.

The truth is credit scores are credit scores. There is no bucket for the black sheep that declared bankruptcy and a separate bucket for those that were responsible with their credit. That just wouldn’t make sense.

Credit scores are impacted by different factors from public records to length of credit history and credit inquiries. That allows all scores to be compared to one another in one bucket.

Here’s what likely happened

It’s a pretty solid assumption that those who have filed for bankruptcy aren’t great at managing their credit. It’s also likely that filing for bankruptcy doesn’t change these people’s habits. Sure, in some cases it hopefully does (like mine). But how many people do you think file for bankruptcy and immediately go back to living beyond their means as soon as they have the chance?

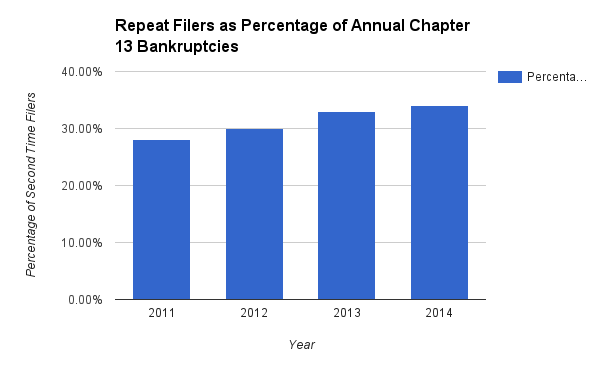

Well, some data from the United States Court can help shed some light on that. There were 301,103 chapter 13 bankruptcies filed in 2014. Of that number, 34% were repeat filers! That means over one-third of those bankruptcies were people who had filed bankruptcy in the last eight years.

Wow!

The numbers don’t look much better for years I could find data. In 2013, 33% of all chapter 13 bankruptcies were attributed to second time filers. That number was slightly lower in 2012 at 30%, and a bit lower at 28% for 2011. But that’s still incredibly high. Clearly, people aren’t learning their lesson.

And while most people file chapter 7 bankruptcy, it’s likely safe to assume there’s little change in the numbers. What’s even more frightening to think about is these are the number of people that treated their finances so poorly they had to file bankruptcy a second time.

How many people do you think are in poor financial shape and haven’t filed a second time? Also note that these are repeat filers from the last eight years. That says nothing of those that waited more than eight years to file bankruptcy again.

Why credit scores really dropped

If you haven’t already figured it out, here’s what I’m getting at…

All those people posting in forums broadcasting cautionary tales of their credit score dropping after their bankruptcy removed likely never changed their habits. Chances are these people continued abusing credit cards and living off debt, but did not become repeat filers.

A bankruptcy removal from your credit score is not an automatic green light for a huge credit bump. If you continue taking credit for granted and abusing it after your bankruptcy, you’re going to be in for a rude awakening when that bankruptcy finally falls off your credit.

Instead, shape up! Reform your life and start rebuilding credit like I did and be rewarded with an 803 credit score when your bankruptcy is finally removed (true score was later pulled for a mortgage refinance and came in at 803!).

But does this explain everything?

Listen, I’m not claiming to be a credit expert. I can only share my story and what I did to rebuild my credit. I knew I never wanted to be a slave to my poor credit score so I got with the program. Does it ever make sense that a bankruptcy removal would result in a lower score? I really don’t see how, but again… I’m not an expert.

Maybe accounts that were included in the bankruptcy were also removed. That could drastically affect the average length of credit, one of the factors that your score is based on. Maybe these people had some recent derogatory marks that were the real culprits of their score drop. I have no clue. The point is, your score should definitely go up substantially if you were responsible rebuilding your credit after bankruptcy.

I hope that by showing you my real life example it can serve as a beacon of hope for those waiting for their bankruptcy to be removed. I sure would have appreciated a detailed answer like this rather than depressing forum posts from years ago.

If you’re rebuilding your credit, start monitoring it for free with CreditKarma. It’s a lifesaver, and I don’t know what I’d do with out it.

Awesome explanation Travis. I am 5+ yrs down and waiting. It’s going well so far. Thank you for your time and this article. 🙂

Half way there, Dianna! I’m glad to hear it’s going well. Just keep it up and you should see a nice big bump like I did.

Thanks for your explanation. Mine will be removed this December. I have 4 credit cards and I just paid all off to a 0 balance. I’m hoping to see a nice jump as well.

Hi Kebra, hopefully you’ve been good with your credit up to this point. Four credit cards seems like a lot to me. I only have one. If you’ve been opening a lot of credit accounts and carrying large balances you may not see the same results as I did.

Thanks. I had them opened since 2014. I don’t carry large balances. I’m in the process of getting a mortgage, so my loan officer said it was good. I have a total of 4k in cc debt. But, all paid to a 0 balance.

What does the score go up to?

Did your credit score go up?

Glad I found this! And you hit the nail on the head about people with lower scores after BK came off.

I checked my credit karma today. But what I saw was weird! I had filed BK Nov 2007. Equifax removed my BK (wasn’t there yesterday), and my score went up 76 points. But, here is the weird part, Trans Union DID NOT remove my BK.

How is that possible? Just random that they didn’t remove it? I see the picture in your article showed both changed at the same time.

I’m not sure if I need to call Trans Union or just wait this out another couple of weeks. I’m not planning on getting or needing to apply for anything anyway, especially since I froze all my reports ?

Hey Survived. First, congrats on the jump in the credit score. Seems you’ve been a good consumer these last 10 years 🙂

That is strange that Equifax did not remove your BK. Who knows what the issue could be. With the recent hack of user data, there’s no telling…

That said, I’d give it a couple weeks to see if it adjusts. If not, definitely get in touch with them or even file a dispute to alert them it should have fallen off by now.

Thanks! I was careful the last ten years ?

Actually it was Trans Union that didn’t remove it. Equifax did. Wondering if they are more likely

To remove closer to the actual filing date. I’ll be checking every day even though it’s a weekly update. ?

Thank you for responding!

So I just got a very nice surprise!!!

I just check Credit Karma and Trans Union updated. My Trans Union score went up 81 points and my Equifax went up another 2! Now I just need to see what Experian has.

Thanks for the advise. It was just the answer I was looking for

Filed BK in Feb ‘09, currently have a 698 score. Looking forward to this coming off and putting this behind me in 15 months or so.

I’ve seen ads for Lexington Law stating they can have a CH 7 BK romved earlier than 10 years, but I’d be wary to try this, since the process requires disputing accuracy of filing and having a 30 day period to to close dispute (which I’m guessing they are gambling the time would run out prior to receiving verification which makes the process possible).

I thought about trying it but decided I’d ride out the clock on this

Thanks for your insight

Hi Micahel,

The last couple years are the most irritating. You’re almost there, congrats!

I tried Lexington Law earlier on to help get my credit back in shape. They weren’t able to get rid of my bankruptcy (obviously), but they did help with some other issues. That said, it’s nothing you can do on your own (as you likely know). I wouldn’t expect them to help much with the bankruptcy, that’s a tough one. Good news is you’re almost there.

Better days are ahead, my friend.

My chapter 13 fell off my experian and my score jumped up 80 points. Transunion only 38….and will come off Equifax in 6 weeks.

This is a ridiculous post because you’re talking about the useless VantageScores from Credit Karma which aren’t used by ANY consumer lenders to gauge creditworthiness.

If you pulled your FICO scores, you may see a point drop. The posts at MyFico and elsewhere reference FICO credit scores, which are typically the “real” scores that lenders use. No consumer lender users Vantage Scores, those are purely educational entertainment value numbers that don’t always align with reality.

Thanks for your opinion, Adam. I’m aware that CreditKarma isn’t a “true” credit score, but in my experience it has always tracked it very closely. In fact, when I applied for (and received) my home loan ~6 months ago, my true credit score was a hair over 800. So there’s definitely correlation between CreditKarma and your credit scores. It’s a great way to track your credit without having to pay for an expensive service.

Actually…….

I track my credit using multiple scoring methods.

Credit Karma is reliably about 20 points lower than the actual score lenders use. So is Equifax, as an Equifax credit monitoring customer ( what a joke, right? They are the ones that recently breached half of America’s credit) I get free credit scores anytime I want.

Experience was actually the closest everytime my credit has been pulled

Thx Travis,

As I waited anxiously for my FICO scores to reflect my BK falling off I read your post and was nervous about my scores dropping. Experian was first to reflect with an 82 increase and 843 credit score! A month later and Equifax increased to 820. Transunion still isn’t showing but should change some time this month. Thanks for giving me hope prior to the actual changes!

Hey Michelle, I’m glad the post gave you some hope. The last stretch is tough to get through! Glad to hear the scores have moved up. Seems you’ve been diligent over the years. Nice work and keep it up!

Thanks for the info. I saw the same comments about people’s scores dropping after their BK dropped off. I’ve got about 7 months to go but for some reason I haven’t been able to get mine above 698. No matter what I do that’s the highest it goes. I do have several store cards from stores we shop at often. Mainly because they offer discounts and other incentives to use them. But I always pay them off when I use them. I got upset with the car dealership when I bought my car because I specifically asked them not to shop my loan for the best rate and just use Ford credit. But they shopped it anyway and insisted that it wouldn’t hurt my credit score. But it did! Now I’ve got 4 inquiries on my report. I hear that some lenders don’t take them into account when they are all close in dates, but it still affects my score. We are looking at refinancing our house soon. We were just waiting for the bankruptcy to fall off first. Hopefully it will have positive results.

Hi Charly, that’s exactly why I wrote this post. You’re already anxious enough to have your bankruptcy drop off, no need to get paranoid too! I wouldn’t worry too much about the inquiries. As you probably know, they’re not a huge factor on your credit report, especially compared to public records like a bankruptcy. Good luck with the refinance. I’m betting you’ll qualify for a great rate.

Travis, thank you for the well thought out explanation. I have been chipping away at bringing my score back up as much as I can. I was active duty Army with almost fifteen years of service with a credit score of around 830 when in 2014 they reduced the forces and I was out of a job. Lost my car, my house, and had to declare chap 7. My score fell over 200 points down to about 605 at its lowest. I am back up to 715 but was worried when I saw stories of scores dropping after they remove the record. Hoping someday to get back to where I was before. Thanks again!

Hi Jeffrey, sorry to hear about your struggles. You have a much better excuse than I do for having declared bankruptcy! I was just plain young and stupid.

Sounds like you have awhile yet before it drops off, but that’s great you’ve already managed to improve your score so much. I’m not sure I was able to get mine much above the low 700’s until the bankruptcy came off. So you might be stuck there for awhile, but it’s really a decent score still. And the more distance you put between “today” and the bankruptcy the better things look to creditors.

Stay disciplined and stay patient. Hope things have turned up for you!

Good discussion – thanks! I just passed the 7 year mark after filing Chapter 7 and wouldn’t have noticed it except for a Credit Karma msg saying my credit score had gone up. Since I haven’t done anything unusual credit-wise lately to change my score in either direction, I checked it out. After they showed my TU score increasing 53 points and my Equifax score increasing 60 points, I felt compelled to find out why. I know from past research that Chapter 13 ‘s are removed after 7 years and Chapter 7 ‘s after 10 years. So the 7 year mark shouldn’t have changed anything according to that rule. So I researched if further and found an Equifax article that explains it very clearly. My scores went up because although the BK filing itself doesn’t come off for another 3 years, all debts that were included in the filing come off after 7 years.

“While the public record of the bankruptcy may remain on your credit report for up to 10 years, the individual accounts included in bankruptcy remain on your credit report for less time—seven years from the original delinquency date that led to the bankruptcy status.

If one of these items does not fall off your credit report after the time allotted by law, you can file a dispute with one or more of the three nationwide credit reporting agencies (CRAs).”

https://blog.equifax.com/credit/the-state-of-your-credit-report-seven-years-after-bankruptcy/

Interesting, I wasn’t aware of this. I don’t remember having a similar experience, but I may have seen the same thing on my score after seven years. I wasn’t tracking it that close at the time because I’d do everything I could to improve my credit and was just in waiting mode at that point. I’m glad you saw a great bump to your score though. Almost to the ten year mark!

Travis, Thank You! I read 3 poor stories before this one, and this is good news. The bad news for me was I thought it came off after 7!!! 🙁

I’m through 6 solid. I hover between 725-735 from Trans & Equifax. Another 4 years to go. Starting a business currently, and sure wish I could get time off for good behavior! lol

The one area that I can’t get a higher report from is “Credit Age” because of a refinance, early payoff, and CC additions for miles.

Congratulations on your accomplishment, and thank you for sharing your story. FR

Hey Frederick, I’m glad I was able to provide you some good news. Sorry to hear you thought you were almost to the finish line though 🙁

The good news is your score is pretty solid right now. Keep up the good work and these next few years should go by in no time.

I filed in January 2011 so I’m coming up on 7 years. What I found that it’s not impossible to obtain credit soon after. In July 2012 bought a new car (not brand new but a year old). Interest rate wasn’t ideal but after 6 months refinance. That’s now paid off and I’ll drive it into the ground. Nice not having a car payment. The 2 credit cards I do have are aweful though. Low limit, annual fee. Can’t use it for much. I’ll charge gas or groceries and pay them right off on time. I’ve also obtained a small personal unsecured loan for $1500 from a local credit union. They’ve been good to me. I’ve been extremely cautious with credit. Maybe almost too cautious because I’m afraid that eventually once everything falls off there won’t be enough reportable accounts to base a good credit score on. I’ve seen my score go from low 500’s right after Chapter 7 to 687 now. Trying to crack 700 seems impossible. I do find that the further away from the Bk I get the less impact it has. I just refuse to apply for credit if I don’t have to.

Side note: 2 of my scores are close to the same, but Experian is 40 points lower. No surprise there. I can’t believe any reputable bank or lender could ever trust that company again after that data breach.

So I have so many questions … So filed in Jan 2012 for CH 7 BK but now I am stuck with a low credit score of 540. I was able to buy a new car in 2016 with a car loan. But after look at my credit report I see 34 inquiries which they will all fall of by June 2018. I NEED HELP with boosting up credit .

And do know have many points it will go up after the inquiries drop off

I too filed in Jan 2012, but a Chapter 13. I didn’t find out until almost 2 years ago that I could start rebuilding before the discharge. I joined 2 separate credit unions and from each I did a secured loan (acts as a pseudo installment loan) and a secured credit card (1 $300 limit and 1 $500 limit). My score increased by an average (3 bureaus) of 68 points within 3 months. Then steady small increases for another 6 months. Started out in low 600s in April 2016 and have been stuck in the low 700s for about a year now. Long story short – – – Credit Union is Our Friend!

Nice tip regarding the credit union route, Tim. I wish I’d been more proactive rebuilding my credit early on too. That’s hindsight, I suppose. Looks like you’re about where I was now… treading water until that bankruptcy drops off. It will be here before you know it though!

I did the exact same thing only I waited 1 year into my 5 year plan. I am still currently in chapter 13 and I have about 3 years to go.

2 different credit unions – both of them I took $1000 shared loans out on

1 of them I got a $1500 secured credit card

1 of them actually gave me a $500 unsecured credit card.

I was allowed up to $2000 in credit without trustee approval and allowed to keep

100% of my tax refunds…

my scores started at around 540 – 575……within 6 months of low utilization and on time payments all 3 of my scores jumped about 50 points.

I am actually going to rinse and repeat on both credit unions as they both are allowing me to get a normal signature loan for $2500. I don’t intend on using any of the money. I am going use it to pay the loans themselves.

hopefully by the time I do reach discharge I can be close to the 700’s ….only time will tell.

That’s a great way to rebuild some credit history, Tim. Nice work, keep it up!

i too had read all the horror stories on the other boards,how my score was going to take a nose dive once the bkk had fallen off my credit report. my score in late December was a respectable 705 on Equifax, and then the day came on Jan 02 when i updated my report. my score went from 705 to 778…from good to excellent..i was stocked…i’m still stocked!

i believe it’s like Travis said the people who saw their score decline were the ones who just continued to abuse their credit and didn’t learn any lesson at all from their bankruptcy.

Happy New Year everyone! I filed bankruptcy in December 2007 and have since rebuilt my credit score. My bankruptcy will fall off in December 2018. I now have a credit score of 749 Experian; 745 TransUnion; and 747 Equifax. I also have 9 credit cards (2 Chase, 3 AMEX, Discover, Wells Fargo, Citibank) all with high credit lines from $20,000 to $35,000, and an installment loan. I got to this point by requesting credit line increases every six months, I charge between $1-2 per month on each card. The Chase card was the hardest to get due to my bankruptcy. After being denied I called and spoke to a representative explaining how after filing I learned to become more responsible with my finances. Before filing I had low budget credit cards. Now I have credit cards that offer higher rewards. One thing I learned is that you have to be responsible and have it in your mind that you are not going to overextend yourself. I don’t use credit cards for charging but for purchasing power instead. For example before it used to take me over half a day at a car dealer to purchase a car. A little less than a year ago I was able to go to a reputable dealership and due to my credit and researching of interest rates, I told the dealer the interest rate that I was not going above and that I only wanted my credit pulled once. In an half hour I was able to leave the dealership WITH the car that I went in for at the rate I requested. Please let me know if you have any questions or comments! Thank you.

Boy am I glad to see this article and subsequent comments. I too use Credit Karma and saw the same thread, which sent me into a slight panic. My Ch 7 is due to reach its 10 year maturity in August, and I’ve been working diligently to improve my scores via helpful sources like Credit Karma and Magnify Money, etc. I went from a 500~score to today’s which is mid 700’s by having 100% payment history, low utilization (only slip slightly north of 30% around the holidays, then pay that down during tax/bonus season), increased overall credit availability from about 2K post bk to 25k today, keeping hard inquiry’s to no more than 2 at a time, and having no other derog. remarks/accounts outside of the bk.

The (fingers crossed) bump in credit score will be most helpful as I’d like to purchase my first home in 2019. I also plan to refi student loans (post-bk debt to get a well worth it masters) so the credit score bump will hep there as well.

One of the biggest challenges I’m facing now, is the credit I procured post-bankruptcy, is at quite high interest rates. While the accounts have received consistent increases in credit limits, the interest rates still hurt in terms of new debt. If I understand the system correctly, new creditors can see the rates I’m carrying, which may lead them to offer me high rates as well, despite my drastically improved credit scores now vs. when those accounts were opened. Going to approach my current creditors (most of which are 7-10 year old accounts) and request rate reductions. That would also potentially help the student loan refi and home purchases – 2 long term debts that interest rates will significantly impact!

Gyda, it sounds like you’re doing all the right things. Way to be on top of it! I hope you’re well in position to purchase your home next year.

Thanks for the post, My bk is no longer in experian but it is still on the other 2 and my score jumped up 15 points, after the bk we have been paying off the credit cards every month and paid with debit most of the time.

Hey Sam, sorry I’m late to this. Hopefully your bankruptcy is completely nuked by now!

Thank you for writing this article. I’ve also read the horror stories you’ve mentioned.

I’ve got 2 long years to go. I’m most concerned about my length of credit history. Credit Karma shows it at just under 5 years and only lists open accounts. Nothing but time can fix that.

In 2016 I refinanced my house that was purchased in 2012, two years after bankruptcy. I currently have 50% equity. I have a good mix of credit. One mortgage, one Visa card with a $14K limit, and never used over 10%, one store card that is over 10 years old, zero balance, New car (6 year) loan, about to be paid off 2 years early. I only owe $800 bucks.

My CK scores currently 740-744. 100% on time payments. It had been stuck between 720-730 for the past year or so. I’m hoping to get up to 760 over the next 2 years before the BK comes off. Really looking forward to putting this behind me and I’m crossing my fingers for a boost when the BK drops off. Prior to the BK my score was 790.

The BK was filed jointly. Now my credit is all individual.

My personal tip: Run a credit report on anybody you plan to marry. Their debt becomes your debt.

Hey Phoenix, great tip for everyone. It’s not very romantic, but it’s your life. You can always prolong marriage until your potential spouse gets their credit back in good shape. I wouldn’t worry too much about the credit history. My wife and I don’t have that many accounts, so when we opened our new home loan last year our average age of accounts went back under the 5 year mark. Our scores are still in the 790’s. So this isn’t a huge contributing factor from my experience.

Thanks for writing this article. My BK was filed in September 2009 and I was essentially looking to see if it drops off the CR 10 years after filing or after when it was closed. Seems that its supposed to fall off 10 years after filing, I too was also wondering how much a credit score might go up, and at least your article gave some info on what tends to happen. I did accumulate more debt again but its manageable and not out of control. The main reason I had to file a BK in 2009 was bcoz I went through a divorce and literally got stuck with the all of the debt from both myself and my ex-wife AND I lost my job and could not find another one that paid anywhere near what I had been getting paid previously (thanks recession). Anyway, looking forward to a positive bump in my score in 9 months even if it won’t be a huge one!

Rick,

Sorry to hear you were stuck between a rock and a hard place. But 9 months… you’re so close! Congrats!! And yes, as long as you’ve been responsible since your bankruptcy in 2009, you should see a nice bump to your score. BTW, we just had our credit pulled for a home equity line of credit application and I’m now sitting at a 817 score. That’s three points higher than my wife’s came in at 🙂

Discharged in August 2013 and so I’m about halfway to the 10 year mark. Vantages Score puts me around 710 as of 1/1/2019. I read somewhere that that the effects of each derogatory item on your credit report has less and less impact with time. If so, maybe that is why some people report little or no change once the removal date finally comes? I’m hoping for a huge positive impact once my day arrives. Fingers crossed.

Hey Shaun,

I can’t say for 100% certainty, but yes, it makes sense that derogatory items would have a lesser impact over time. That said, a bankruptcy is a huge blemish. While its impact may reduce over time, having it come off should always result in a positive signal assuming you’ve been responsible with your credit.

Best of luck to you!

My Chapter 7 ten year mark is next month! Stay tuned for my score increase or decrease. Anxious but I know it’s not the end of the world either way. Fingers crossed.

Wow, Justin! Congrats!! I hope you drop by here and let us know what happens.

On April 29, 2019 my wife and I will hit our 10 year mark for filing chapter 7 bankruptcy. Our scores have been in the 710-720 range for the last few years. We each have one credit card, with a $5,000 credit limit, and our payment record has been 100%. We pay off the entire balance every month, and the balance never goes above 20% of the limit. My wife’s credit history is about 8 years old, and mine is about 3 years old. We have a car loan with Toyota Finance that is 18 months into a 4 year length at 1.9%, with perfect payments. That’s all we have. We own our house with no mortgage. What do you think? Will we get a bump? I assume my wife’s score will go up more than mine because of the length of her credit. Thanks for anyone’s input or opinions. 10 years is a long time.

Hi Fred,

If I had to guess I’d say yes, you’ll absolutely get a bump. Your situation sounds a lot like mine was (although I wasn’t married). It sounds like you’ve done all the right things and truly seems like you’re a changed man. Congrats!

If I had to guess, given your current scores, you’ll probably see a move into the high 700’s.

Let us know what happens come April 29th!